The Icarus Intelligence Problem

Intelligence is being created faster than anyone can figure out how to own it. Including the people creating it.

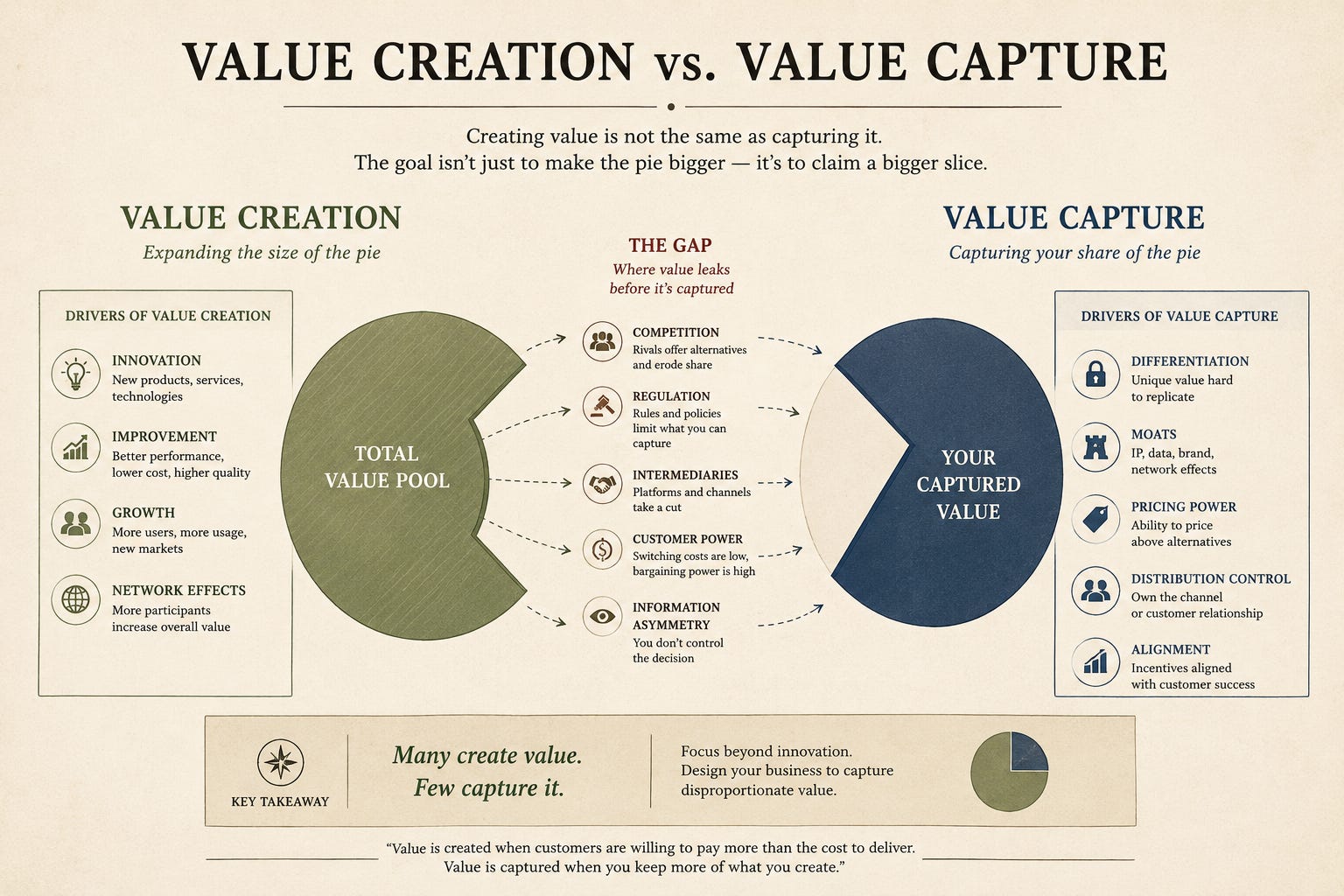

In Business Innovation & Strategy the first thing worth learning is that value creation and value capture are not the same thing.

As a consultant I was often tasked with estimating value. How much of the market could my client take based on x price, for y volume. Right, now how much of that could they realistically actually achieve vs. competition?

Research into pioneer advantage suggests first-mover failure rates near 47%, against roughly 8% for fast followers. The companies that dominate a category are rarely the ones that invented it. Google wasn't the first search engine. The iPhone wasn't the first smartphone. Pioneers absorb the force; fast followers ride the slipstream.

I keep coming back to this because we are inside the largest value-creation event ever recorded, and far too few are taking the capture question seriously in discourse (the only one I saw recently hint at this was Scott Galloway).

AI as the Fifth Leverage

Naval Ravikant once described four forms of leverage: labour, capital, code, and media.

“Fortunes require leverage. Business leverage comes from capital, people, and products with no marginal cost of replication (code and media).”

The first two are classical. The second two are what made the last twenty years of internet wealth so plentiful. One person with code can serve a million users. One person with media can reach a million minds. Neither requires permission.

AI, through its ability to do work with Claude Code, Codex etc.) has just become the fifth form of leverage, yet the point many miss is that it is weirdly also a multiplier on all four: It makes labour more productive, capital more targeted, code cheaper to write, and media cheaper to produce. It is the most asymmetric tool anyone in the history of commerce has been handed.

Which, in theory, is wonderful. Genuinely, historically wonderful.

Hollowed from Above… and Below

The labs are shipping so much capability into their base products that whole categories of SaaS are becoming redundant by-products. The market has noticed: Salesforce -34.5% YTD, Workday -41.8% (as of 15 May 2026).

A single person with Claude Code and a weekend can now ship the v1 of a product that used to need eighteen months and a seed round. First-party coding agents replace three categories of developer infrastructure at once. OpenAI says this out loud. Anthropic does it more quietly: keep the protocols open (MCP), go scorched earth on the application surface.

But the labs are not as safe as their valuations imply. Open-source weights - DeepSeek, Kimi, Qwen - are no longer eighteen months behind the frontier. They are closer to six, and closing. Frontier intelligence is not a decade-long moat. It is a quarter or two, then someone releases weights 85% as good, free, private, and local — a devastating competitor to 100% but remote, metered, and surveilled.

The under-priced twist: by shipping Claude Code, agents, and skills, the labs are arming their most capable customers with the exact tools needed to build the thing that replaces them. The recent leak of Claude Code’s internals made the point concrete. The harness, the scaffolding, the agent loops, the architectural knowledge that separated frontier labs from everyone else, is now in the open. This has never been true in a prior platform shift. Microsoft did not ship Office’s source code to ISVs.

The Subsidy Is Thinning

If you are an SaaS builder, founder, or investor reading this, you already know. You can feel the terminal value of the next decade getting shorter every quarter.

The latest real example of this is a friend who started an AI financial planning startup. They’re now in the crosshairs of OpenAI’s new financial planning feature for Pro users:

Meanwhile Anthropic recently tried to quietly remove Claude Code from its $20 Pro plan for new users. GitHub briefly paused Copilot signups. The cover story in both cases was usage. The real one is that intelligence is expensive, and venture subsidy is thinning on all accounts, and the moment the compute bill lands on the customer rather than the investor is approaching.

Icarus

This is not anyone’s plan. Each player is doing something locally rational. Labs ship to justify rounds. Incumbents bolt on AI to defend revenue. Open-source teams release frontier-adjacent weights to recruit talent. Each feather is fitted with care. The aggregate is an ascent toward a sun no one on board has priced in.

So what?

Value creation is racing ahead of value capture on every front. The labs are creating more value than they can keep. SaaS is losing it faster than it can rebuild. Users are getting more capability than they’ve paid for.

The answer is to not despair that “SaaS is dead” - it’s not. Solving problems for people is never dead. The trick is in learning how to capture the value the big guys are leaving on the table.

The durable bet is to own as much of what you create as you can: your memory, your data, your distribution. And when the AI Labs IPOs land later this year, remember that the companies creating the value are rarely the ones that get to keep it.

Thanks for reading The Wayfinder Notes. If this resonated, would love you to hear your thoughts and comments.

Value creation versus value capture is such a great framework!

The first-mover's advantage is one of those concepts we hear all the time and internalize as a fundamental fact, so this was such a fascinating wake-up call to how AI flips that into a liability.

Great read and equally great insights!

Great article man, actually interesting which is rare to find

Subscribed, would love to have you along too🙂